Team AcumenSphere

|Last Updated: July 10, 2026

|Publish Date: July 10, 2026

Learn why a 409A valuation is often lower than a post-money valuation. Understand common stock pricing, preferred shares, pre-money vs. post-money valuation, and what it means for founders and employees.

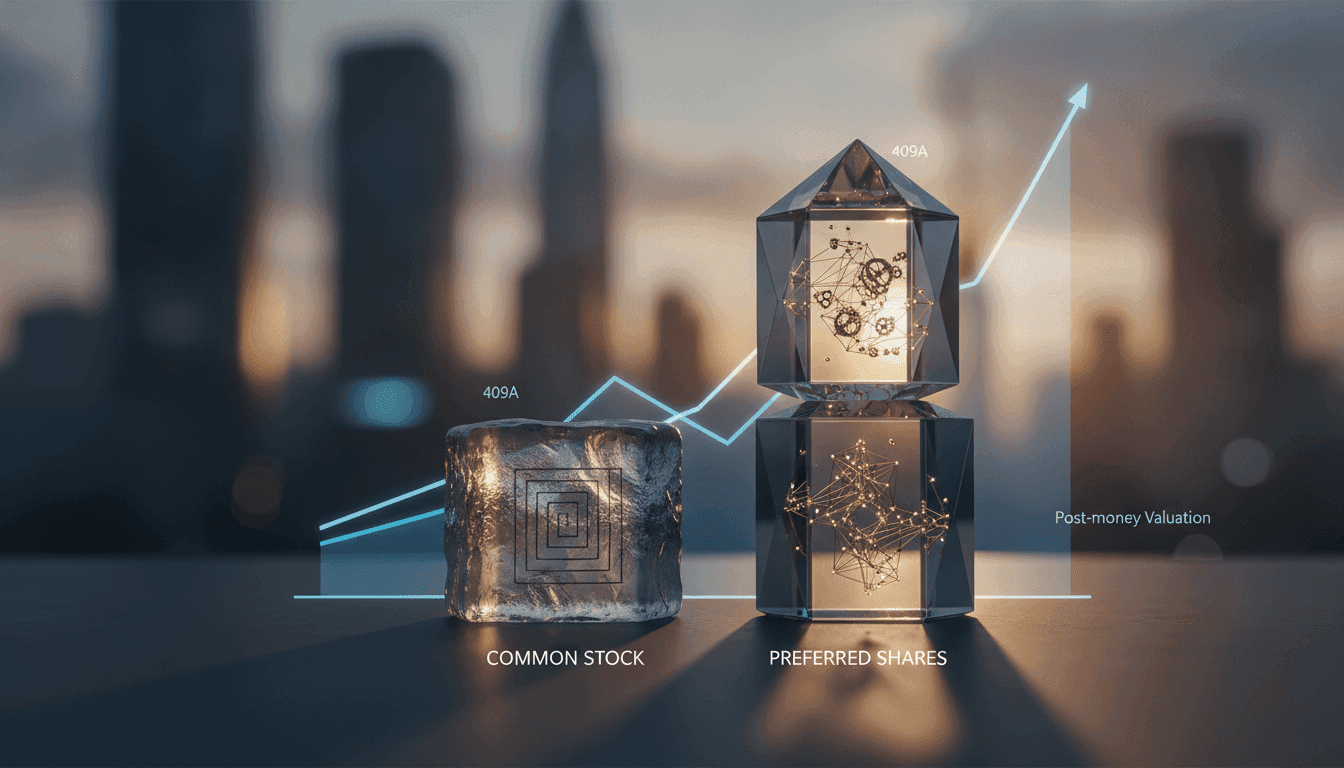

You've just closed a funding round, and investors have paid $10 per preferred share. A few weeks later, your independent 409A valuation arrives, showing that your common stock is worth only $4 per share. If you're wondering whether your company's value suddenly dropped, you're not alone—and the good news is that it almost certainly didn't.

This difference is completely normal. A 409A valuation determines the Fair Market Value (FMV) the price your common stock would reasonably sell for in an open market for employee stock options and IRS tax compliance. A post-money valuation, on the other hand, reflects the price investors paid for preferred shares during your latest funding round. Since preferred shares come with additional rights and protections, they are generally worth more than common stock.

Understanding why these two values differ helps you make better decisions about fundraising, employee equity, and tax compliance. It also helps you confidently answer questions from your team when they notice that the option exercise price is much lower than the price investors recently paid.

Feature | 409A Valuation | Post-Money Valuation |

|---|

Purpose | IRS tax compliance | Fundraising |

Share Class | Common Stock | Preferred Shares |

Prepared By | Independent valuation firm | Investors & founders |

Used For | Employee stock options | Investment pricing |

Regulatory Basis | IRS Section 409A | Venture financing |

Key Takeaways

Different objectives: A 409A valuation establishes IRS-defensible FMV for common stock and stock options, while a post-money valuation reflects the negotiated enterprise value implied by a priced round of preferred equity.

Capital structure matters: Preferred shares typically carry liquidation preferences, anti-dilution protections, and other rights that justify a higher per-share value than common stock when allocating equity value across the cap table.

Safe harbor protection: A robust, independent 409A valuation helps your company achieve IRS “safe harbor” status under Section 409A, materially reducing the risk of adverse tax consequences for employees and founders.

Pre-money vs. post-money: Pre-money and post-money valuations are investor-facing constructs that drive dilution and ownership percentages; they are not a substitute for a formal 409A analysis.

Strategic timing: Significant events—new financing, secondary sales, or performance inflection points—often require a refreshed 409A valuation to keep option pricing defensible and aligned with current facts and circumstances.

What Is a 409A Valuation and Why Does It Focus on Common Stock?

A 409A valuation is an independent appraisal of the fair market value of a private company’s common stock, used primarily to set exercise prices for stock options and other deferred compensation subject to IRS Section 409A. It is required when granting options to employees, advisors, and other service providers to avoid punitive tax treatment if options are deemed “in the money.”

Under IRS Section 409A, equity awards with an exercise price below the FMV of the underlying common stock at the grant date can be treated as nonqualified deferred compensation subject to immediate income inclusion, a 20% additional federal tax, and potential interest penalties for the recipient. A defensible 409A valuation provides a framework to establish FMV of common stock using accepted valuation methods and to create a “safe harbor” presumption that the exercise price is compliant.

Source: According to IRS Section 409A and related Treasury Regulations, nonqualified deferred compensation arrangements must generally value underlying equity at fair market value at the time of grant, and a valuation performed by an independent appraiser using reasonable methods is presumed reasonable unless shown to be grossly unreasonable.

What Is a Post-Money Valuation and How Is It Determined?

A post-money valuation is the negotiated value of a company immediately after a financing round, calculated as the price per share paid by new investors multiplied by the total number of shares outstanding on a fully diluted basis after the investment. It is an investor-facing figure that reflects capital deployed and ownership percentages, not necessarily the FMV of common stock.

In venture financings, investors negotiate a price per share for preferred stock that embeds expectations about growth, risk, and exit potential. That price, multiplied by fully diluted shares post-closing, yields the post-money valuation. This construct is central to dilution modeling, board discussions, and investor reporting, but it does not automatically equate to the fair market value of every class of equity in the cap table.

Why Is the 409A Valuation Often Lower Than the Post-Money Valuation?

The 409A valuation is frequently lower than the headline post-money valuation because it specifically values common stock after accounting for the superior rights and preferences of preferred shares. Valuation professionals allocate the company’s total equity value across different share classes using methodologies that recognize liquidation preferences, participation features, and conversion rights.

Key drivers of this difference include:

Liquidation preferences: Preferred investors typically receive their invested capital (and often a multiple) back before common holders receive any proceeds in a liquidity event.

Downside protection: Anti-dilution provisions, protective covenants, and seniority among preferred series shift economic value away from common stock.

Lack of control and marketability: Common shares usually have fewer rights, no guaranteed exit, and are subject to significant transfer restrictions, warranting discounts for lack of control and lack of marketability.

Option value vs. headline value: The post-money figure embeds optimistic forward-looking expectations; the common stock FMV reflects current risk-adjusted economics, not just the last round’s marketing narrative.

Why a $10 Preferred Share Can Result in a $4 409A Valuation

Imagine you've just raised your Series A funding.

An investor purchases preferred shares at $10 per share, giving your startup a healthy post-money valuation. A few weeks later, your independent valuation provider completes a 409A valuation and determines that the fair market value (FMV) of your common stock is $4 per share.

At first glance, this may seem worrying.

"Did my company just lose 60% of its value?"

The answer is no.

The investor purchased preferred shares, which include additional protections such as liquidation preference (meaning investors are typically paid before common shareholders if the company is sold), anti-dilution protection (which helps preserve their ownership if new shares are issued at a lower price), and other contractual rights.

Your employees receive common stock, which doesn't include those additional protections.

Because these two share classes offer different economic benefits, they are expected to have different values—even though they represent ownership in the same company.

For your employees, this is actually good news. A lower 409A valuation means a lower exercise price—the amount they pay to purchase their shares. If your company grows over time, they have the opportunity to benefit from a larger increase in value.

Myth vs. Reality: Understanding the Difference Between 409A and Post-Money Valuation

It's common for founders to compare their latest funding valuation with their new 409A valuation and assume something has gone wrong. In reality, these valuations answer different questions and are designed for different purposes.

Myth:

A lower 409A valuation means my startup has lost value.

Reality:

Not at all. A 409A valuation estimates the fair market value of common stock for tax compliance, while a post-money valuation reflects what investors paid for preferred shares. A lower 409A valuation is expected and doesn't mean your business is worth less.

Myth:

Employee stock options should be priced at the same value investors paid.

Reality:

Investors buy preferred shares with additional rights and protections. Employees receive common stock, which has different rights. That's why employee stock options are typically granted at a lower price.

Myth:

A lower 409A valuation is bad for employees.

Reality:

Quite the opposite. A lower fair market value (FMV) generally results in a lower option exercise price, allowing employees to purchase shares at a lower cost and potentially benefit more if the company's value increases in the future.

Myth:

My latest funding round automatically becomes my new 409A valuation.

Reality:

Your recent financing is an important input, but an independent 409A valuation also considers your company's financial performance, market conditions, capital structure, and the different rights attached to each share class.

How Do Valuation Specialists Bridge Preferred and Common Values in a 409A Analysis?

Valuation specialists typically start from an enterprise value informed by financing rounds, market comparables, and discounted cash flow models, then use structured allocation methods to derive a value for common stock. These methods explicitly recognize that preferred shareholders sit ahead of common holders in the capital stack.

Common allocation approaches include:

Option Pricing Method (OPM): Treats each class of equity as a call option on the company’s equity value, with liquidation preferences serving as strike prices. This is often used for earlier-stage companies with significant uncertainty about timing and outcomes.

Probability-Weighted Expected Return Method (PWERM): Models multiple exit scenarios (IPO, strategic sale, downside exit) with probabilities and allocates expected proceeds based on capital structure terms. More common for late-stage companies with defined exit paths.

Hybrid methods: Combine OPM and PWERM when certain exit scenarios are more visible but material uncertainty remains.

These frameworks frequently show that while the preferred share price from the last round may be a reasonable starting point for total equity value, common stock often supports a materially lower per-share FMV once preferences and risk are fully modeled.

How Do Pre-Money and Post-Money Valuations Relate to 409A Valuations?

Pre-money and post-money valuations are negotiation anchors between founders and investors and are not substitutes for an independent 409A valuation. While the last round terms inform a 409A analysis, they cannot be used mechanically to set common stock FMV without considering capital structure and rights.

In practice:

Pre-money valuation: The agreed value of the company’s equity immediately before new capital is invested, based on the negotiated preferred share price and fully diluted shares outstanding pre-financing.

Post-money valuation: The pre-money valuation plus new capital invested, or equivalently, preferred share price multiplied by fully diluted shares outstanding after the round.

These figures are useful for understanding dilution and investor ownership but are only one input into a 409A valuation. A compliant 409A analysis must consider all relevant facts and circumstances, including financial performance, market conditions, and rights attached to each class of equity.

What Are the IRS Safe Harbor Rules for 409A Valuations?

The IRS provides “safe harbor” presumptions under Section 409A when a company uses a qualified, independent appraisal or certain formula-based approaches, shifting the burden of proof to the IRS to demonstrate that the valuation is unreasonable. Relying on a safe harbor framework substantially mitigates the risk that equity awards will be treated as discounted options.

To access safe harbor protection, companies typically:

Obtain a valuation from an independent appraiser with significant experience and appropriate credentials.

Ensure the valuation uses recognized methods and reflects all material information about the company’s financial condition and prospects.

Refresh the valuation at least every 12 months, or sooner if a material event occurs, such as a new financing round, major acquisition, or significant business inflection.

When Should You Update Your 409A Valuation After a Financing Round?

You generally need a new 409A valuation when there is a material change in your company’s value or capital structure, including a significant equity financing. Relying on a pre-round 409A valuation after a major financing event can undermine safe harbor status and invite scrutiny.

Common triggers for a refresh include:

Closing a new preferred equity round or significant convertible instrument conversion.

Signing or losing a material customer, launching a transformative product, or entering a new market.

Executing or terminating major strategic partnerships or acquisitions.

Receiving a bona fide acquisition offer or preparing for an IPO process.

For fast-growing companies in ecosystems like Silicon Valley, New York, or Austin, where valuations can change quickly, many boards standardize on quarterly or semiannual reviews if there is frequent option grant activity.

What Does a Lower 409A Valuation Mean for Founders and Employees?

A lower 409A valuation isn't something to worry about. In most venture-backed startups, it's a normal outcome because common stock and preferred shares have different rights and are valued differently. For founders, it supports compliant employee stock option grants. For employees, it often means a lower exercise price, making equity compensation more valuable if the company continues to grow.

Strategic implications include:

Talent attraction and retention: Competitive option pricing can materially improve the perceived value of equity compensation, especially for key hires comparing offers across high-growth tech companies.

Tax exposure management: A defensible 409A valuation reduces the risk that options will be recharacterized as deferred compensation with adverse tax consequences under Section 409A.

Board and audit oversight: Boards and audit committees increasingly expect documented methodologies and independent third-party support for equity valuation assumptions used in financial reporting and compensation decisions.

How Should You Explain the Gap Between 409A and Post-Money Valuations to Your Team?

You should clearly communicate that the post-money valuation is an investor-oriented, headline figure based on preferred share pricing, while the 409A valuation is a technical assessment of common stock FMV for tax compliance. The gap between the two is a function of capital structure, rights, and risk—not a sign that investors or employees are being misled.

Effective talking points include:

Preferred stock has economic and control advantages that common stock does not, which justifies a higher per-share price.

The 409A valuation is designed to protect employees from adverse tax treatment by aligning option exercise prices with IRS-compliant FMV.

Both numbers can be “right” for their respective purposes: one for fundraising narratives and investor reporting, the other for tax and accounting compliance.

Securing Defensible Valuations with AcumenSphere

Regulators, external auditors, and sophisticated investors increasingly scrutinize private company valuations, especially where equity compensation, cross-border entities, or complex capital structures are involved. A weak or poorly documented 409A valuation can expose your organization to IRS challenges, financial statement adjustments, and erosion of employee trust.

Based in California’s Bay Area, AcumenSphere’s US-based team of credentialed specialists—CPAs, CFAs, and professionals holding valuation designations such as ABV®—delivers audit-ready 409A, ASC 805, and ASC 820 valuations tailored to venture-backed and cross-border enterprises. Our frameworks integrate your latest financing terms, cap table dynamics, and financial performance to produce defensible, well-documented conclusions that stand up to due diligence and regulatory review.

To discuss your upcoming valuation requirements or review your cross-border compliance framework, schedule a consultation with our US advisory team. We help founders, CFOs, and boards align option pricing, financial reporting, and tax compliance with the expectations of the IRS, auditors, and institutional investors.

Final Thoughts

If your 409A valuation comes in lower than your latest post-money valuation, don't assume your startup has lost value. In most cases, you're simply looking at two different measurements created for two different purposes.

A post-money valuation reflects what investors paid for preferred shares during a funding round, while a 409A valuation determines the fair market value of common stock for employee stock options and IRS compliance. Both figures can be correct at the same time.

Once you understand the difference between pre-money valuation, post-money valuation, and 409A valuation, you'll be better prepared to communicate with employees, investors, board members, and auditors while making confident equity compensation decisions.

Need Help with Your 409A Valuation?

Whether you've recently completed a funding round, are preparing to issue employee stock options, or need to refresh an existing valuation, obtaining an accurate and independent 409A valuation is essential for tax compliance and informed equity decisions. Understanding how post-money valuation differs from common stock fair market value helps founders avoid confusion and communicate equity more effectively with employees and investors.

At AcumenSphere, our valuation professionals work with startups, venture-backed companies, CFOs, and founders to deliver independent, audit-ready 409A valuations that align with IRS requirements and industry best practices. We help you navigate complex equity structures with confidence, ensuring your option pricing remains compliant and well-supported.

Ready to discuss your valuation needs?

📞 Phone: +1 (925) 399-7268

📧 Email: info@acumensphere.com

Or contact our team to schedule a consultation and learn how we can support your next funding round, employee stock option plan, or annual valuation update.